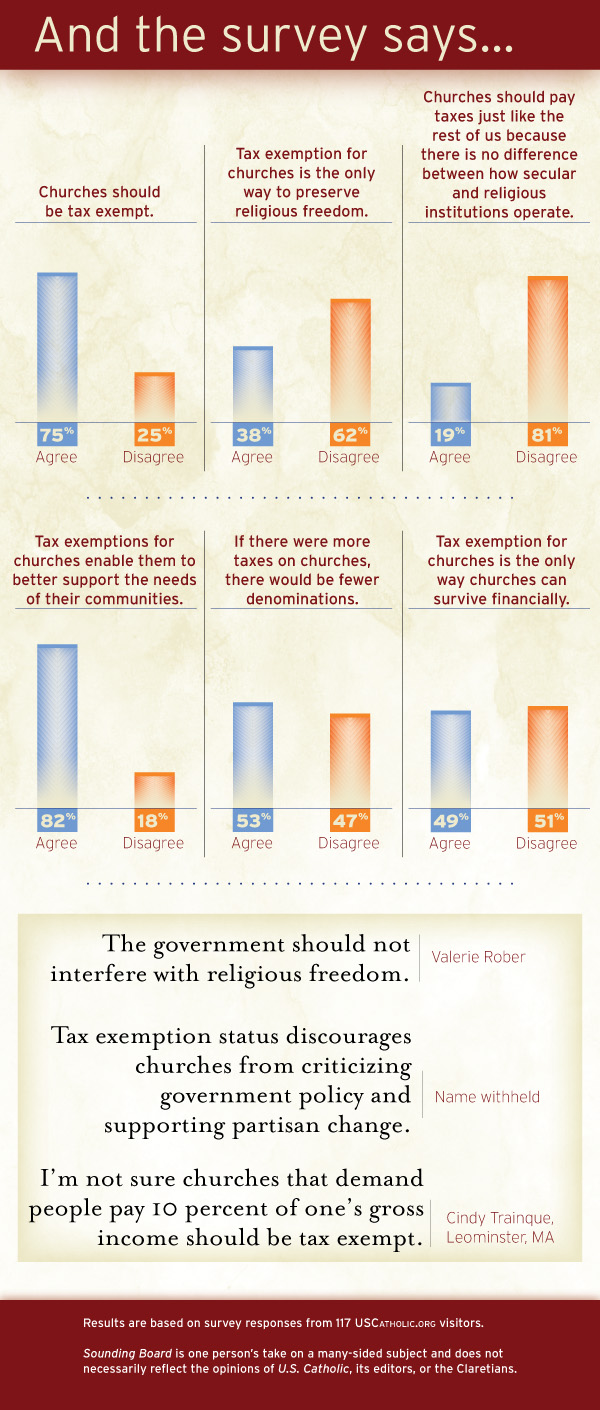

During the oral arguments in the Supreme Court’s 2015 case dealing with the legal recognition of same-sex marriages, an exchange between Justice Samuel Alito and Solicitor General Donald Verrilli stirred up some controversy. Alito had asked whether religious institutions that refuse to recognize same-sex marriages would lose their tax-exempt status. “It is—it is going to be an issue,” Verrilli said.

Columnist Mark Oppenheimer took it a step further when he insisted that the Supreme Court ruling had made it “clearer than ever that the government shouldn’t be subsidizing religion and non-profits” and that it was time for churches “to pay their fair share.”

In the United States, churches and other religious institutions are, generally speaking, exempt from federal, state, and local taxes. They have been for a long time. This deeply rooted practice is good policy and helps to promote and protect our fundamental right to religious freedom. After all, that right includes the right of religious believers to act in and through religious institutions, so it makes sense to protect those institutions from the intrusions and burdens of tax laws.

Some argue, however, that this exemption is unjustified. Perhaps even more noteworthy than Oppenheimer’s comments was Last Week Tonight host John Oliver’s scathing take down last year of IRS rules and practices having to do with religious organizations, including his own (short-lived) church, “Our Lady of Perpetual Exemption.”

But our tradition of exempting churches and religious institutions from taxes is justified and important. The separation of church and state is not a reason to invalidate or abandon these tax exemptions but is instead a very powerful justification for retaining them.

The Supreme Court’s precedents and popular opinion have been shaped, for better or worse, by Thomas Jefferson’s figure of speech about “a wall of separation.” This saying has often been misunderstood and misused. Still, Jefferson’s metaphor points to an important truth: In our tradition, we do not banish religion from the public square, and we have not insisted on a rigid, hostile secularism that confines religious faith to the strictly private realm. We do, however, distinguish between political and religious institutions. They can productively cooperate without unconstitutional entanglement.

Some argue, though, that tax exemptions for churches undermine Jefferson’s “wall of separation” between church and state because they inevitably require government officials to make tricky judgments about what is and isn’t religious. And then there are those who are less impressed by the good works that churches are thought to do and who emphasize instead the scandals, intolerance, and ignorance of the religious. As the late Christopher Hitchens might have put it, “religion poisons everything.” So why should we reward it with special tax treatment?

Others argue tax exemptions for religious institutions (and tax deductions for contributions to them) amount to unnecessary and unjustifiable public support for what should be private activities. Organized religion is on the wane, it is said, and there is no reason for government to prop up the organizations and practices of religious people who worship in sanctuaries as opposed to those of “spiritual” people who express their no-less-worthy commitments in other ways. And still others point to the billions of dollars that the exemptions and deductions are said to drain from the public coffers. Why provide this special (and costly) treatment to churches and their supporters, the argument goes, when there are potholes to fill, firefighters to pay, and pensions to fund?

Of course, tax exemptions and deductions of all kinds can be, and are, manipulated and abused. Not all religious institutions contribute to the common good, not all religious beliefs are inspiring, and not all religious believers are generous. Nevertheless, the First Amendment’s prohibition on “any law respecting an establishment of religion” is a crucial safeguard for religious freedom that should be carefully and consistently enforced.

Nearly 50 years ago, in a case called Walz v. Tax Commission of the City of New York, the Supreme Court considered a challenge to the city’s property-tax exemptions provided to religious organizations for “properties used solely for religious worship.” The challenger said the exemption required him to contribute money to religious institutions and therefore violated the Constitution. The justices rejected this argument for reasons that are still compelling today.

For one thing, as the Court observed, churches’ tax-exempt status neither advances nor inhibits religion. Religious institutions are not singled out with a special status; instead, they are treated as part of broader class of nonprofit associations. (This is also true today.) As Chief Justice Burger wrote, the government considers these groups as “beneficial and stabilizing influences in community life and finds this [tax-exempt] classification useful, desirable, and in the public interest.”

This policy is consistent with Americans’ longstanding habit of forming and joining groups and working together on common projects. We have always believed that what social scientists call “mediating institutions” play a vital role in our communities. They train us for citizenship, they bring us together through cooperative ventures, they limit the danger of government overreach, and they facilitate healthy diversity, experimentation, and competition. It makes sense for governments to exempt voluntary associations—like churches—from taxes because it makes sense for governments to promote a thick and vibrant civil society.

The Walz Court also noted that tax exemptions safeguard against any hostility toward religion—which is frequently economic, political, and sometimes harshly oppressive. “Governments have not always been tolerant of religious activity,” the justices reminded readers.

There are also many good policy reasons for exempting churches, faith-based homeless shelters, parochial schools, and religious hospitals from taxes. Many of these reasons also apply forcefully to cultural, artistic, and social welfare agencies of all kinds. It is a good thing to have a vibrant, diverse, and competitive civil society, to support rather than resist pluralism, to increase rather than shrink the opportunities for engagement with others, and to avoid monopolization by governments of too many activities. There are things that, probably, only governments can do, but there are many more things that non-state agencies can do, too, and better.

But these policy justifications are not the whole story. A political community like ours, that is committed to the freedom of religion and appropriately sensitive to its vulnerability, takes special care to avoid excessively burdening these institutions or interfering in their internal religious matters. It’s not that churches’ contributions to the public good make them deserving of a tax-exempt status; it’s that, given our First Amendment, secular power over religious institutions is and should be limited. Governments refrain from taxing religious institutions not because it is socially useful to “subsidize” them but because their power over these institutions is limited—and because “church” and “state” are distinct.

The point of church-state “separation” is not to create a religion-free public sphere. It is, instead, to safeguard the fundamental right to religious freedom by imposing limits on the regulatory—and, yes, the taxing—powers of governments. After all, as Daniel Webster famously argued in the Supreme Court (and the great Chief Justice John Marshall agreed) the power to tax involves the power to destroy, and so we have very good reasons for exercising that power with care—especially when it comes to religious institutions.

This article also appears in the October 2016 issue of U.S. Catholic (Vol. 81, No. 10, pages 19–22).

Image: Flickr cc via Ken Teegardin